JOHCM Global Select Strategy

Size

GBP 961.35m

Artificial Intelligence (AI), weight-loss therapeutics (GLP-1), and de-globalisation are rewiring global macroeconomic frameworks, disrupting many industries, and altering the foundation of corporate profits. This is driving significant stock dispersion within the traditional equity factors of growth, value and quality, making them misleading and less useful to investors.

The winners and losers from AI, GLP-1 and de-globalisation have made some parts of the traditional growth universe resemble value stocks (e.g. software and media); some parts of the traditional value universe resemble growth stocks (e.g. banks and commodities); and many traditional quality stocks are seeing their previously solid business models fundamentally challenged (e.g food and beverage).

AI is not just a tech-sector phenomenon, it is reshaping many industries by driving massive capital expenditure into the physical economy while disrupting many traditional business models. The economic impact is highly uneven, creating winners who boost productivity across all sectors, and losers who fail to secure a return on their AI investments or get left behind. AI is likely to have a similar impact on many industries as Amazon had on retail, disrupting incumbents, compressing margins, and forcing businesses to reinvent themselves or risk irrelevance.

The rapid adoption of GLP-1 weight-loss drugs represents a massive, idiosyncratic lifestyle and consumer behaviour shift. By altering consumption patterns, these therapeutics are challenging traditional consumer staples and healthcare businesses, while simultaneously expanding opportunities in specialised wellness, fitness, nutrition and healthcare service providers. Perhaps the greatest irony of the GLP-1 revolution is that Novo Nordisk, the company that sparked it, now looks more like a value stock than a growth stock. Despite operating in one of the fastest-growing segments of global healthcare, a series of management mistakes has left investors questioning whether the company’s growth potential is being fully realised.

The shift from globalised, just-in-time supply chains towards more resilient, onshored, just-in-case production models has increased business costs and challenged the long-term profitability assumptions underpinning some multinational companies. Yet, this structural realignment is also creating significant domestic investment opportunities. As governments increasingly prioritise economic security, they are directing capital towards domestic infrastructure, energy independence and strategic industries, often supported by local financing channels.

At the same time, access to critical commodities is becoming a matter of national security rather than simple economic efficiency. In this environment, selected financials, industrials and commodity producers should no longer be viewed solely as traditional value stocks; they are emerging as beneficiaries of powerful long-term growth trends.

As a result, the traditional boundaries between growth, value and quality investing are becoming increasingly blurred, as AI, GLP-1s and de-globalisation reshape earnings growth expectations across industries and geographies. It makes sense to us that the traditional definitions of growth, value and quality are being challenged. Our process is based upon our belief that share prices tend to follow (or lead) changing earnings growth expectations, not labels. As one of our mentors taught us, “growth investing only works if you avoid growth traps (i.e. growth disappoints), value investing only works if you avoid value traps (i.e. structural deterioration), and quality investing only works if you avoid quality traps (i.e. fundamental disruption).”

The definition of growth is always changing, just ask the horse, the canal, the railroad, the car, the plane, and the soon to be IPO’d SpaceX. The early stages of the AI boom created a hardware arms race, in which the previously “cyclical growth” semiconductor sector became perceived as a “structural growth” sector.

As the AI investment boom matures, the market will probably remember that semiconductors are cyclical after all, and pivot to adjacent AI growth sectors. So far, many leading AI companies have stayed private for much longer than usual, starving the public equity markets of their growth. This will soon change with the trillion-dollar IPO’s of SpaceX, Anthropic, and OpenAI, who will all become new and large parts of the growth index.

The definition of value is changing. Japan used to be one of the most expensive developed equity markets and currencies in the world, now it is one of the cheapest. Today, the software and consumer staples sectors are well on their way to becoming the new value sectors due to disruption from AI and GLP-1s respectively. Meanwhile, de-globalisation, onshoring and government-backed infrastructure spending are boosting traditional value sectors such as financials, industrials, materials, and utilities. These legacy businesses are not relics of the past; they are helping build the infrastructure of the future. Perhaps investors need a new acronym: VARG = Value at the right growth, in place of GARP. After all, when value stocks become growth stocks, the labels matter far less than the earnings.

Even the definition of quality is changing. Kodak was once considered a textbook quality stock, generating attractive and dependable returns. Then digital cameras arrived, its competitive moat disappeared, and the business collapsed. Today’s quality companies may not be tomorrows.

Many software companies used to be quality businesses, then came AI. Snacking used to be a quality business, then came GLP-1s. Manufacturing in low-cost countries and selling in high-cost countries used to be a quality business model, then came China, Tariffs and de-globalisation.

After the European financial crisis, nobody thought of European banks as quality businesses as their return on equity collapsed to near zero. Today, you might be surprised to learn that the MSCI European Bank index has a higher return on equity than the MSCI USA bank index (13% and rising, versus 12% and not rising) with less private credit issues. The worm has turned as they say, and when the facts change, we change.

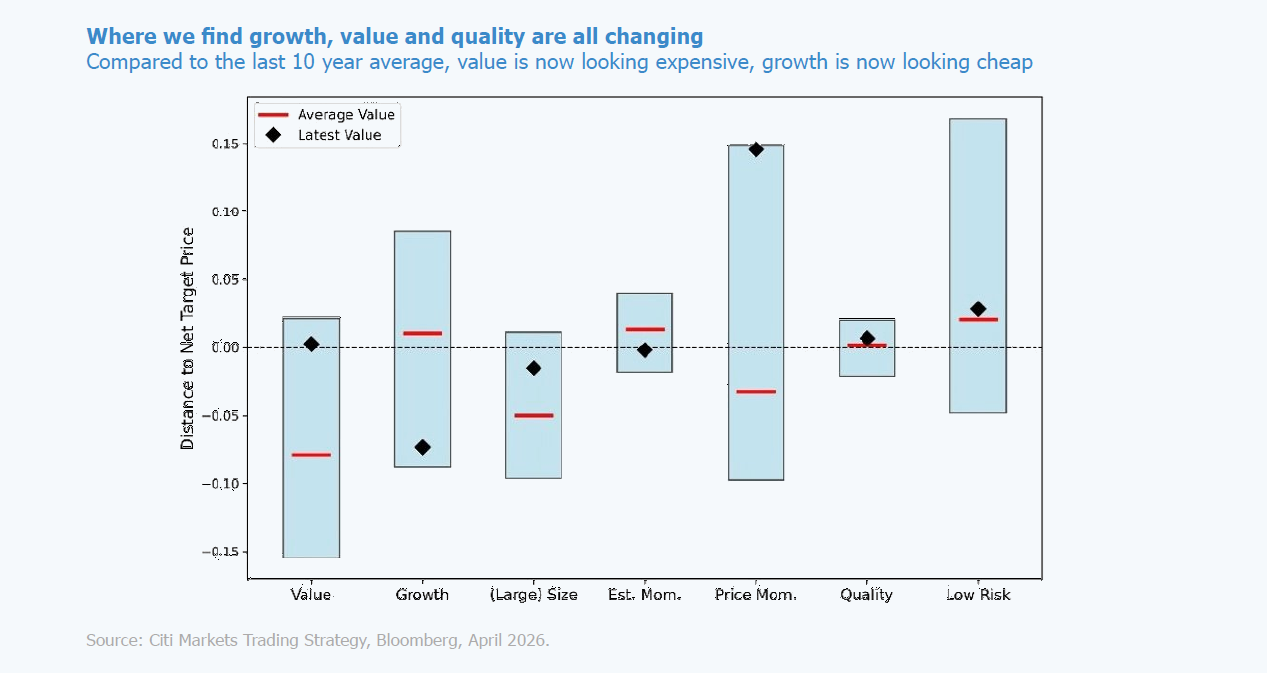

At first glance, this chart suggests that growth stocks look cheap relative to their 10-year history, while value stocks appear expensive. However, we believe both observations are rational. Parts of the traditional growth universe face weaker earnings growth than investors previously assumed and therefore deserve lower valuations. Equally, parts of the traditional value universe are benefiting from improving earnings prospects and therefore deserve higher valuations. The market is not mispricing growth and value, it is redefining them.

The chart also suggests that the traditional quality universe is trading broadly in line with its 10-year average valuation. However, as we have demonstrated, some businesses traditionally regarded as ‘quality’ are structurally losing the characteristics that once justified their premium ratings. As a result, we believe these companies are likely to continue de-rating and trade at lower valuations over time.

Meanwhile, the momentum factor is trading at a significant premium to its 10-year average, leaving this part of the market vulnerable to a correction. We would welcome such pullbacks, as they would provide opportunities to add to positions in companies we believe are long-term beneficiaries of AI, GLP-1s and de-globalisation. We think of these opportunities as ‘early birthday presents’, the chance, we believe, to buy structural winners at more attractive valuations.

In summary, AI, GLP-1s and de-globalisation are changing where investors find growth, value and quality because they are changing future earnings expectations. As these forces create new winners and losers, traditional style labels are becoming less informative. Rather than asking whether a stock is growth, value or quality, investors should ask whether earnings expectations are improving or deteriorating. Ultimately, it is changing earnings, not style labels, that drive stock returns.

Recent tensions in the Middle East have triggered the expected wave of “risk-off” sentiment across global markets. Volatility has spiked and geopolitical headlines dominate the narrative. However, when we step back from the noise, pockets of opportunity stand out.

AI, GLP-1 drugs and de-globalisation are redefining growth, value and quality, creating new winners and losers across markets and reshaping investment opportunities.

Markets may be nearing a turning point as sentiment remains cautious, price action stabilises, fundamentals stay resilient, and light positioning supports recovery via renewed capital engagement.

Our four global investment teams assess the Middle East conflict’s market impact, highlighting risks to energy, inflation and volatility, alongside potential geopolitical scenarios and emerging investment opportunities.

From our very first conversation to ongoing support, our teams of experts are here to answer your investment needs.