JOHCM Global Select Strategy

Size

GBP 961.35m

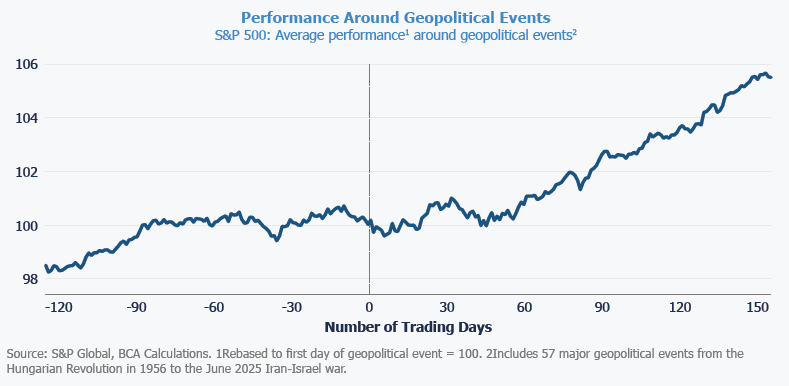

The recent escalation in the Middle East has predictably triggered a bout of “risk-off” sentiment across global markets. Markets often react quickly to geopolitical headlines, but history suggests that the economic and market consequences are frequently less lasting than initially feared. While the humanitarian toll is deeply concerning and the headlines unsettling, our base case remains one of fading geopolitical news.

Speculation around scenarios such as the fragmentation of Iran or rapid political liberalisation appears overstated. A complete breakup of the country is, in our view, a tail risk with extremely low probability, and a swift transition to a democratic system seems equally unlikely in the near term.

If political change does occur, it is more likely to resemble an internal reshuffle of leadership rather than a transformation of the system, a “change of jockeys rather than a change of horse.” At present, however, there is little concrete evidence of such a shift. The defining feature of the current moment remains the fog of war, with information incomplete and speculation abundant.

Recent commentary has questioned whether the Gulf Cooperation Council (GCC) can maintain its reputation as a stable financial hub. We assign a zero probability to such concerns.

The Gulf states retain strong institutional frameworks, substantial financial reserves, and a strategic commitment to economic diversification, all of which provide meaningful buffers against geopolitical shocks.

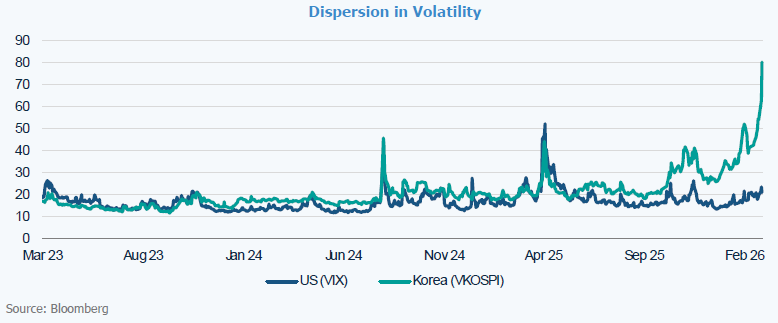

One of the most striking features of the recent sell-off is the geographic divergence in volatility. While the US VIX briefly approached the high-20s during the latest escalation, Asian volatility indices have surged significantly higher. This disparity reflects Asia’s greater exposure to Gulf energy flows, as disruptions to the Strait of Hormuz could affect a large share of oil and LNG exports destined for Asian economies. For investors, this divergence may represent an opportunity rather than simply a warning signal.

The sharp rise in Korean market volatility appears disconnected from the domestic fundamentals. Three powerful structural drivers continue to underpin the investment case:

None of these structural drivers have changed. The recent weakness in Korean equities largely reflects concerns about potential energy supply disruptions rather than deterioration in the country’s economic outlook.

An interesting dynamic during the sell-off has been the behaviour of gold mining equities. Despite gold prices holding relatively firm, consistent with its traditional role as a safe-haven asset during geopolitical stress, gold miners declined. This reflects their equity beta, which often causes them to fall alongside broader equity markets during periods of forced liquidation.

Having entered the episode with strong momentum, mining stocks became an easy source of liquidity for investors seeking to raise cash during the initial wave of panic selling.

Markets are currently pricing in “worst-case” scenarios that we simply do not view as likely. Amidst the indiscriminate selling of high-quality assets caught in the crossfire we are looking for early birthday presents. We are using this volatility to build positions in companies where the market has overreacted and left excellent value on the table. Rather than reacting emotionally to volatility, we remain disciplined and focused on fundamentals.

AI, GLP-1 drugs and de-globalisation are redefining growth, value and quality, creating new winners and losers across markets and reshaping investment opportunities.

Markets may be nearing a turning point as sentiment remains cautious, price action stabilises, fundamentals stay resilient, and light positioning supports recovery via renewed capital engagement.

Our four global investment teams assess the Middle East conflict’s market impact, highlighting risks to energy, inflation and volatility, alongside potential geopolitical scenarios and emerging investment opportunities.

Middle East tensions have shaken markets, but history suggests geopolitical shocks fade. This article explores regional resilience, GCC stability, and investment opportunities created by market volatility.

From our very first conversation to ongoing support, our teams of experts are here to answer your investment needs.