JOHCM Global Opportunities Strategy

Size

GBP 4.66bn

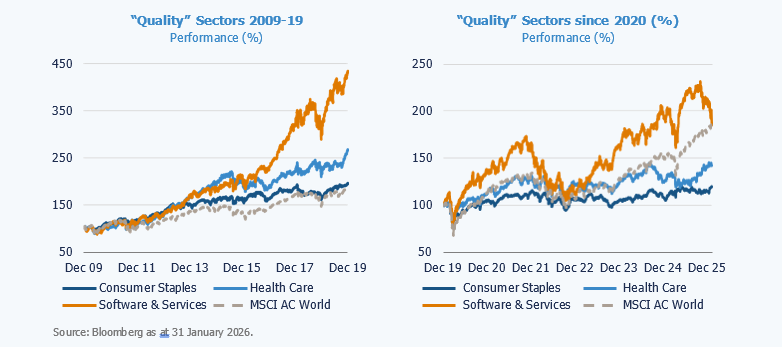

For more than a decade following the global financial crisis, investors took comfort in owning “quality” at almost any price. Capital consistently flowed into consumer staples, healthcare, and software, sectors assumed to offer resilience, pricing power, and durable growth. Over the past three to five years, however, that assumption has been increasingly challenged.

Former quality darlings, first staples and healthcare, and more recently software and information services, have begun to underperform not only tech-led growth, but also traditionally value-oriented sectors such as banks, miners, and semiconductors. As a result, investors are now starting to question whether there is any need to maintain exposure to quality at all.

We continue to believe that quality belongs at the heart of any long-term investment portfolio. It is essential to own businesses with durable franchises, terminal value, pricing power, resilience in the form of low operational gearing and strong balance sheets. Equally important is compounding potential, reflected in the ability to reinvest at high marginal returns on capital. Together, these characteristics should underpin strong shareholder returns over the medium to long term without undue volatility. A barbell approach that concentrates solely on the extremes of expensive growth and deep value is inherently risky and can lead to pronounced volatility at certain points in the cycle.

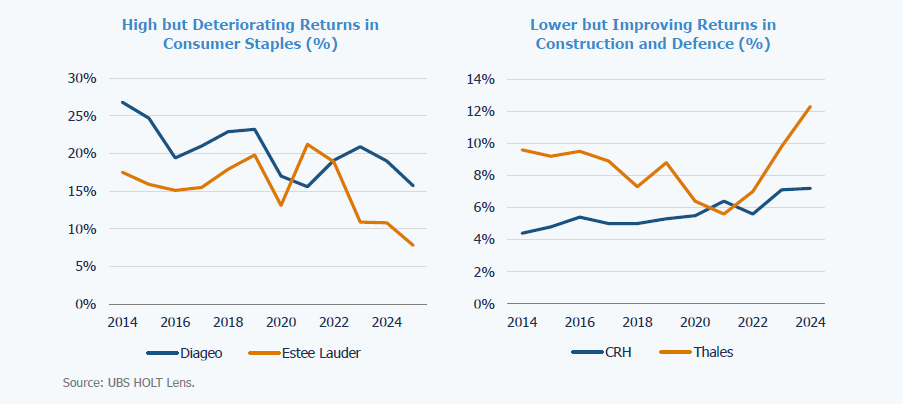

Where we differ, however, is in where investors can find these characteristics. They are not the exclusive preserve of a handful of sectors; rather, they can be found across a much broader range of businesses, provided there is sufficient selectivity. No sector is homogeneous that all its constituents possess these attributes to the same degree. As a result, the emphasis should be on stock selection rather than sector allocation. It is just as flawed to claim that all consumer staples are high quality as it is to argue that all banks are low quality.

One common mistake we see among investors seeking “quality” is the tendency to equate simple, easy-to-screen, backward-looking metrics, such as return on invested capital, with a genuine understanding of the durability of a company’s franchise, which is inherently complex and qualitative. ROIC is, at best, a proxy for quality: it offers clues, but never proof, as to which companies truly possess pricing power, competitive advantage, and the ability to compound over time. We would argue that the direction and rate of change in a company’s return on capital matter just as much as its most recently reported level. In other words, marginal returns on capital can be just as important as historical ones.

At the same time, the world is constantly evolving, and investors must remain alert to how quality can strengthen or erode over long cycles. While higher inflation and AI-driven technological disruption have led to renewed scrutiny of the pricing power and terminal value of certain consumer staples and software businesses, this does not invalidate the broader principle that pricing power and terminal value remain critical components of a resilient investment portfolio.

The final point to highlight is the importance of valuation discipline. Quality characteristics are no guarantee of a great shareholder return. They may underpin confidence in the sustainability of a company’s ability to generate cash or grow its earnings but in the long-term an overvalued asset is never a good investment. The market is starting to recognise that ‘quality at any price’ can be just as uncomfortable as deep value or aggressive growth investing. Quality characteristics must be applied more selectively and complemented by cyclical and restructuring opportunities as markets rotate. This isn’t the time to give up on quality. It’s the time to rethink the old shortcuts, question stale narratives, and take a fresh look at what quality really means and where it’s hiding.

Geopolitical tensions are accelerating investment in energy resilience, creating opportunities across LNG, renewables, nuclear, electrification and domestic energy infrastructure globally.

Our four global investment teams assess the Middle East conflict’s market impact, highlighting risks to energy, inflation and volatility, alongside potential geopolitical scenarios and emerging investment opportunities.

Market leadership is broadening beyond a narrow US-led regime. Rising dispersion and regional divergence are reshaping opportunities and increasing the value of selectivity.

Quality investing is under pressure. We argue it remains essential, but demands selective stock picking, forward-looking analysis, and disciplined valuation in evolving markets.

From our very first conversation to ongoing support, our teams of experts are here to answer your investment needs.