JOHCM Global Opportunities Strategy

Size

GBP 4.66bn

For more than a decade, global equity markets have been defined by concentration. A small group of US mega-cap growth companies delivered most of the returns, rewarded scale over selectivity, and made geographic diversification feel optional. Yet that regime is beginning to reflect crowding and complacency rather than opportunity.

While the Mag 7 fixation endures, opportunities are broadening across regions, sectors, and company size, with return drivers becoming more dispersed. The result is a market where investors have more ways to generate returns beyond a narrow group of crowded stocks.

In this environment, selectivity matters more than company size or benchmark weight. Concentration risk is more visible, dispersion is increasing, and selective global investing has a larger role to play than it has in years.

Concentration does more than skew index returns. It compresses decision-making, channels capital into the same exposures, and raises the cost of being wrong at the margin. When leadership is crowded, small changes in expectations can drive outsized price moves, and correlations can rise precisely when diversification is meant to help.

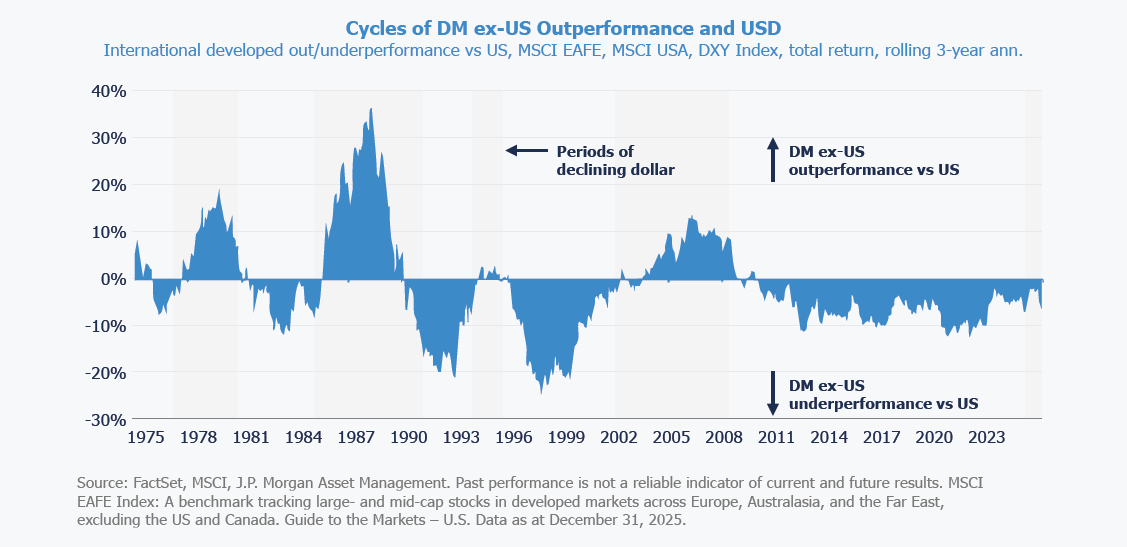

That fragility has become harder to ignore. Recent episodes of volatility have shown how sensitive outcomes can be when positioning is crowded. At the same time, performance outside the US is showing greater differentiation, particularly among small- and mid-cap companies with improving fundamentals.

This divergence matters. It suggests global markets are not always moving as a single trade. Different regions are responding to different forces, creating more scope for stock selection and regional judgment to add value.

The renewed relevance of global equities is not a valuation call or a tactical rotation. It reflects structural changes unfolding unevenly across regions.

In Europe, policy direction is shifting. Germany’s long-standing fiscal restraint is easing, opening the door to higher spending on infrastructure, energy security, and defense. These priorities favor domestic investment and support parts of the economy that were left behind in the previous cycle. Financial institutions are another clear example. After years of regulatory pressure and suppressed profitability, banks in parts of Europe are seeing improving earnings capacity as credit growth resumes and rate conditions normalize.

Elsewhere, Japan is undergoing a quieter but equally important transition. Inflation has returned, interest rates are no longer anchored at zero, and corporate governance reforms are changing how capital is allocated. Many Japanese companies now offer exposure to global demand and structural trends with limited reliance on domestic growth. Volatility around political or policy events may persist, but for active investors, opportunities are increasing. Because they are often earlier in their development and less fully priced, they require active judgment rather than passive exposure.

A widening opportunity set changes the nature of risk. In a narrow market, the greatest danger is missing the dominant trade. In a broader one, the greater risk is failing to adapt as leadership shifts. Diversification in this environment is not about owning more markets indiscriminately. It is about understanding what drives returns in different regions and selecting exposures accordingly. Geographic and sector choices matter again, as does discipline around valuation and expectations.

Some of the most successful companies of the last cycle remain strong businesses. But strong businesses do not always make strong investments if future growth is already reflected in prices. A broader market favors investors willing to move beyond yesterday’s leaders toward new sources of return, even when those opportunities sit away from benchmarks. Volatility is likely to be part of this transition. Not the kind associated with systemic stress, but the kind that creates mispricing. For active investors, patience and selectivity become advantages.

A disciplined global equity approach is well positioned to benefit from regional divergence, sector dispersion, and company-specific change. Doing so demands a clear philosophy, a selective mindset, and a willingness to look beyond the areas traditionally favoured by growth investors.

Many of the most compelling opportunities arise outside the US, particularly where improving fundamentals are not yet fully recognised by the market. Companies in the early stages of growth, those emerging from periods of neglect, or businesses operating in unfashionable segments can offer attractive potential. The emphasis is on identifying change before it becomes consensus.

Geographic exposure is driven by bottom-up opportunity rather than top-down allocation, while sector positioning reflects valuation discipline, earnings momentum, and a conscious effort to avoid crowded trades. In an increasingly fragmented market, this philosophy aligns naturally with the available opportunity set.

Skepticism toward international equities is justified after a long period of relative disappointment for US-based investors. That experience has influenced how investors allocate capital, and their reengagement requires more than near-term performance improvements; it requires a credible explanation of what has changed and why those changes matter for portfolios today.

What has changed is the structure of the market itself. Leadership is spreading across regions and sectors, policy paths are diverging, and corporate behavior is evolving in ways that were largely absent in the last decade. Concentration risk is now visible in market outcomes, and selectivity plays a larger role in determining results. For investors willing to look beyond a US-centric framework, the opportunity set is broader than it has been in a long time. Negative international diworsification has become positive international diversification.

AI, GLP-1 drugs and de-globalisation are redefining growth, value and quality, creating new winners and losers across markets and reshaping investment opportunities.

Markets may be nearing a turning point as sentiment remains cautious, price action stabilises, fundamentals stay resilient, and light positioning supports recovery via renewed capital engagement.

Our four global investment teams assess the Middle East conflict’s market impact, highlighting risks to energy, inflation and volatility, alongside potential geopolitical scenarios and emerging investment opportunities.

Middle East tensions have shaken markets, but history suggests geopolitical shocks fade. This article explores regional resilience, GCC stability, and investment opportunities created by market volatility.

Geopolitical tensions are accelerating investment in energy resilience, creating opportunities across LNG, renewables, nuclear, electrification and domestic energy infrastructure globally.

Our four global investment teams assess the Middle East conflict’s market impact, highlighting risks to energy, inflation and volatility, alongside potential geopolitical scenarios and emerging investment opportunities.

Market leadership is broadening beyond a narrow US-led regime. Rising dispersion and regional divergence are reshaping opportunities and increasing the value of selectivity.

Quality investing is under pressure. We argue it remains essential, but demands selective stock picking, forward-looking analysis, and disciplined valuation in evolving markets.

From our very first conversation to ongoing support, our teams of experts are here to answer your investment needs.